Natural Level of Output

View FREE Lessons!

Definition of Natural Level of Output:

An economy’s

natural level of output occurs when all available resources are used efficiently. It equals the highest level of production an economy can sustain. It is "natural" because an economy returns to its natural level of output following a recession or overheated period. The natural level of output is also referred to as the natural level of production, long-run aggregate supply, or the full-employment output.

Detailed Explanation:

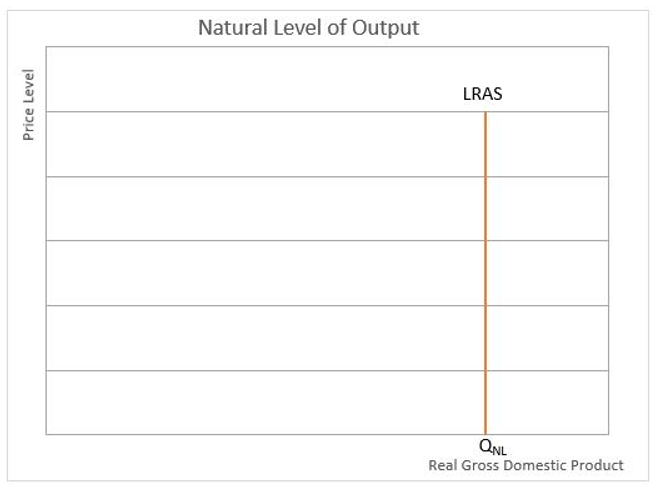

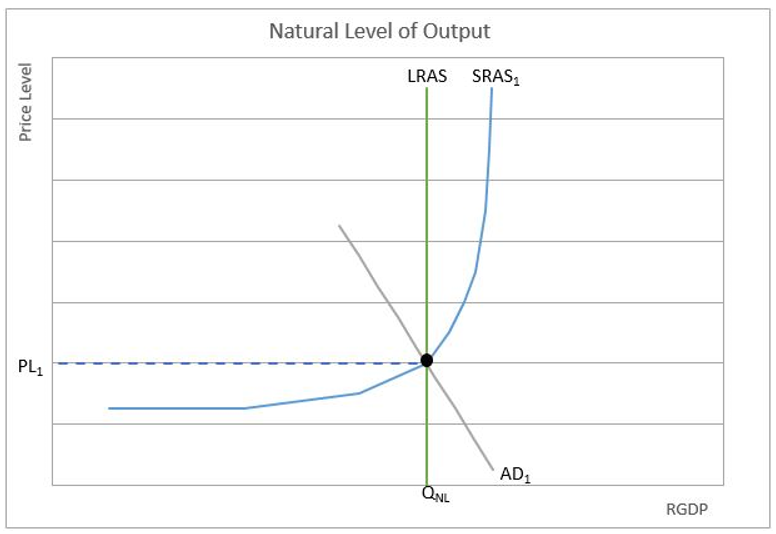

In the long run, an economy that is in a recession or overheated must return to its natural level of production. The economy is at its natural level of production when all the factors of production, including labor, are being used efficiently, but not stretched beyond their capacity. It is where the long-run aggregate supply curve intersects with the x-axis on the graph below.

Graph 1

Why is the long-run aggregate supply curve (LRAS) vertical? When economists refer to the long run they are assuming that all prices are flexible and all inputs are variable. This includes input prices such as labor and raw materials and the prices of the final goods and services. In the long run, an economy’s potential is limited by its factors of production which include its natural resources, people, technology, entrepreneurs, and capital. Note that price is not mentioned. In the long run production is independent of the price level. In other words, whether the price level increases or decreases, the natural level of output is unchanged.

Why is the natural output level independent of the price level?

Production is driven by profits, so we must show that profits do not increase in the long run following an increase in the price level to prove long-run production is independent of the price level.

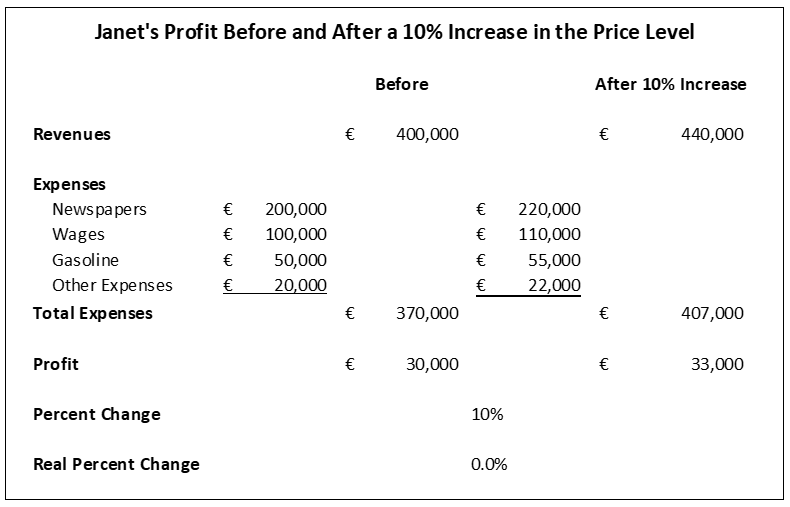

The French company, Janet’s Newspaper Delivery Service illustrates this point. Assume inflation is ten percent, so Janet increases her price by ten percent. The cost of her papers, employees’ wages, rent, gasoline, and all other costs also increase by the general price level, or ten percent. The table below shows the resulting profits before and after the increase in the price level. Janet’s profit increases ten percent, but she is no better off than before because all the prices in the economy have increased ten percent. Her purchasing power is unchanged. Therefore, there is no incentive for Janet to increase her supply. i.e. the number of papers she sells. If we extend this specific example to every business in every sector of the economy, we understand why when all prices increase or decrease by the same percentage, the natural level of output is unaffected.

How does an economy return to full employment output when the economy is in a recession?

Prices and output are flexible in the long run. When something triggers a drop in the economy’s aggregate demand, the price level and short-term output fall –

until the prices of all inputs and outputs adjust. Assume a financial crisis lowers the demand for Janet’s delivery service and she is forced to lower her prices ten percent. Initially, she is very reluctant to decrease the amount she pays her employees, and gasoline prices remain unchanged. Profits decline, so she is willing to supply fewer newspapers at a lower price. However, in the long run, prices and wages adjust. Some employees may accept a ten percent reduction in pay. Others may be let go since she sells fewer newspapers. Gasoline prices match the ten percent decline in the price level. The reduction in her costs boosts profits so she is again willing to provide the same number of newspapers as before. The economy has returned to the full employment level of production, but at a lower price level. This is illustrated with the series of graphs below.

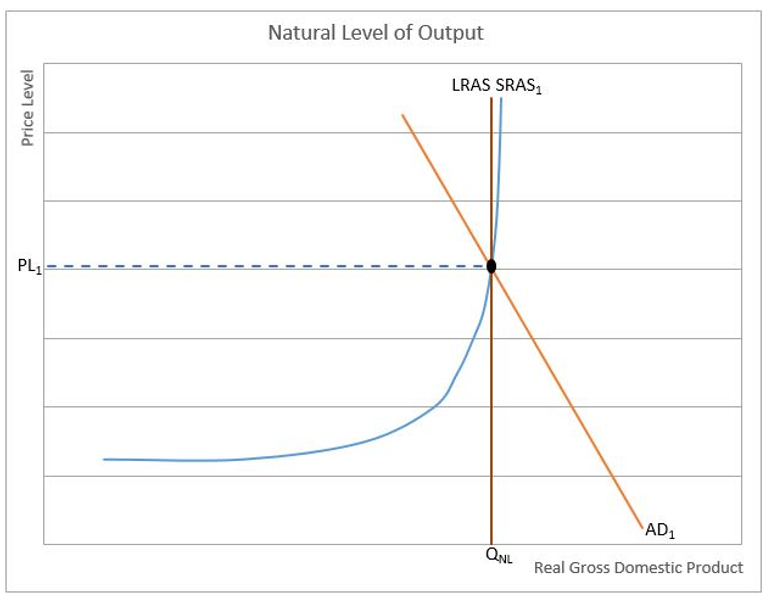

Initially, the economy is operating in a long-run equilibrium where the short-run aggregate supply (SRAS), LRAS, and aggregate demand (AD) are in equilibrium and the resulting price level is PL

1 and Q

NL is the RGDP.

Graph 2A

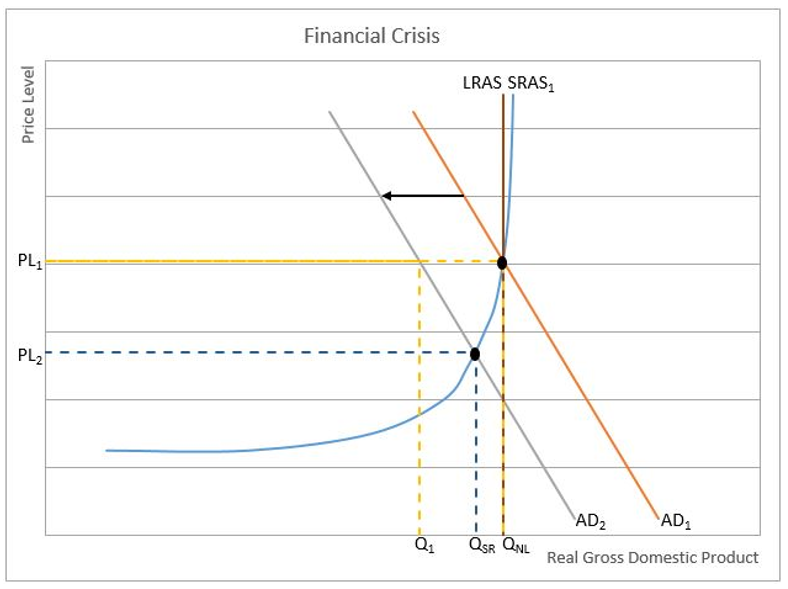

Assume a financial crisis triggers a drop in the aggregate demand (AD) from AD

1 to AD

2. Shortly after, companies see the demand for their goods and services decrease. The output would fall to Q

1 if the price level remained at PL

1, but companies respond by lowering their prices hoping to increase the quantity demanded for the good or service they offer. Because they are unable to reduce all their costs, production still falls, but not to the same degree it would without reducing prices. In the short run, there is movement along the SRAS from (PL

1, Q

NL) to (PL

2, Q

SR). A short-term equilibrium is reached where the price level is PL

2 and production falls to Q

SR.

Graph 2B

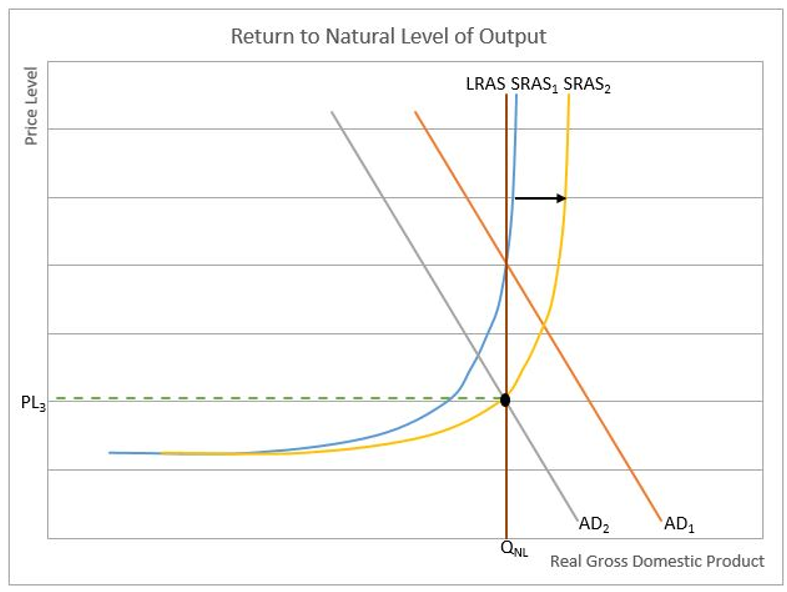

At this point some employees have lost their jobs, and the demand for other inputs has decreased because production in the economy has fallen. All producers are benefiting from a lower cost because the decrease in demand for inputs has resulted in a lower input cost, which causes a rightward shift of the economy’s short-run aggregate supply curve to SRAS

2. Employees are rehired, but at a lower wage, which in theory they do not mind since the economy’s price level has also decreased. In the long run all prices in the economy decrease by the same percentage. Eventually, long-run equilibrium is reached where the output returns to its natural level, Q

NL, and the price-level drops to PL

3. This illustrates how an economy returns to its natural level of output following a financial crisis.

Graph 2C

How does an economy return to its natural level of output when the economy overheats?

When the economy is operating at its long-run equilibrium all resources are being used at the full employment or natural production rate. Resources are not pushed beyond the point where prices are dramatically impacted. Economies can be compared to long-distance runners. Long-distance runners are most efficient when they pace themselves. They can sprint for short periods but tire and ultimately hurt their performance if they do so for too long. Like long-distance runners, an economy is most efficient when it paces itself. For short periods, an economy can operate beyond its natural level of output. Economists use similar terms such as “tired,” “overheated,” and “spent” to describe an economy in this phase. During these periods, manufacturers may defer maintenance to continue meeting demand. Workers may tire and become less productive when working overtime for extended periods. Companies raise prices to reduce their quantity demanded. Initially, profits rise, but in the long-run wages will increase because the demand for workers has increased and employees work overtime. Raw materials also become more expensive because of mounting demands. Eventually, the prices of all inputs increase. The higher costs return profits to normal and output is cut back to the natural level of output but the price level has increased.

Let us return to when the economy is operating in a long-run equilibrium. The short-run aggregate supply (SRAS), LRAS, and aggregate demand (AD) are in equilibrium and the resulting price level is PL

1 and Q

NL is the RGDP.

Graph 3A

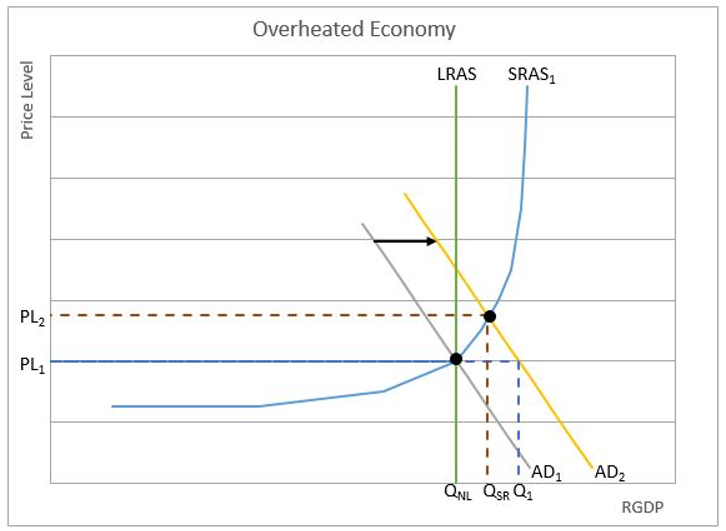

Assume an overheated economy increases the aggregate demand from AD

1 to AD

2. Shortly after companies see the demand for their goods and services increase. Note that if the price level remained at PL

1 output would increase to Q

1. Companies respond by increasing their prices hoping to take advantage of the increase in demand. However, their marginal costs are also increasing. In the short run, there is movement along the SRAS from (PL

1, Q

NL) to (PL

2, Q

SR). Companies increase production and increase their prices to meet the increase in demand. A short-run equilibrium is reached where the price level is PL

2 and production increases to Q

SR.

Graph 3B

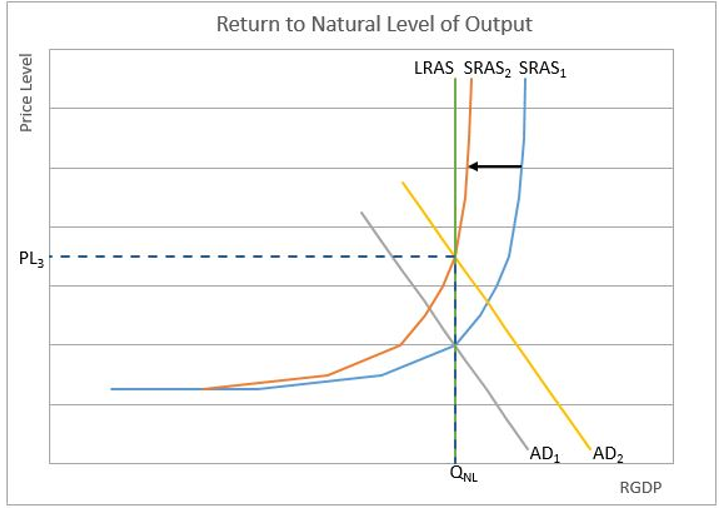

At this point, employees are working overtime and more are being hired. Suppliers are having trouble meeting the company’s increased demand. The forces of an increase in demand and a decrease in the available supply of inputs have pushed the production cost higher, which shifts the short-run aggregate supply curve (SRAS) to the left, to SRAS

2. Eventually, a new long-run equilibrium is reached, resulting in the same production as before, Q

NL, but a higher price level, PL

3. This illustrates how an economy cannot sustain production beyond its natural level of output.

Graph 3C

Dig Deeper With These Free Lessons:

Aggregate Supply – Relating Inflation and ProductionAggregate Supply and Demand – Macroeconomic EquilibriumFiscal Policy – Managing an Economy by Taxing and SpendingFactors of Production – The Required Inputs of Every Business