A depression is the severest form of recessions.

Economic activity fluctuates over time. Usually, a country’s economy grows, and output measured in its gross domestic product increases. However, it is normal for economies to undergo periods of decline in economic output, known as recessions. During a recession, there is a noticeable drop in sales, leading businesses to cut back on production. This, in turn, results in lower profits, layoffs, and increased business failures. Unfortunately, the economic output may continue to decline because unemployed workers have less to spend, prompting businesses to cut back further. To attract more customers, companies may lower their prices. Eventually, the economy starts to recover, but if a recession persists for several years with significant hardship, it may be considered a depression. (There is no specific point at which a recession turns into a depression.)

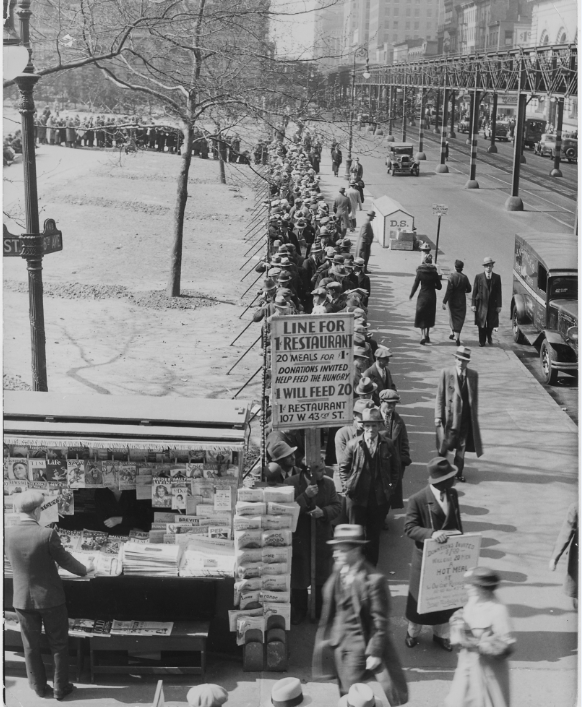

Since 1900, the United States has experienced only one major depression: the Great Depression of the 1930s. This economic downturn began in August 1929 and saw real gross domestic product (GDP)—the most common measure of economic output—fall by 27 percent by 1933. Nearly 25 percent of American workers lost their jobs during this time. The lowest point in the business cycle, the trough, was reached in 1933. Economies around the world were also affected.

After 1933, production began to rise slowly, but it was not until 1936 that production levels returned to what they had been before the Depression. Companies were hesitant to hire, resulting in persistently high unemployment rates. Employment levels did not fully recover until World War II.

Governments use fiscal and monetary policies to stimulate the economy by increasing government spending, reducing taxes, and adjusting the money supply to lower interest rates. John Maynard Keynes developed Keynesian economics during the Great Depression to explain the economic downturn and propose a solution to overcome it. Keynesians advocate for increasing aggregate demand through government spending during recessionary periods to help the economy recover more quickly. President Franklin Roosevelt supported Keynesian policies by implementing the New Deal, which most economists believe played a significant role in helping the United States recover from the Great Depression. Additionally, the increased spending to finance military efforts in World War II further boosted aggregate demand. Keynes’ ideas continue to influence policymakers today.

Business Cycles

The Federal Budget and Managing The National Debt

Fiscal Policy – Managing an Economy by Taxing and Spending

Gross Domestic Product – Measuring an Economy's Performance

Monetary Policy – The Power of an Interest Rate