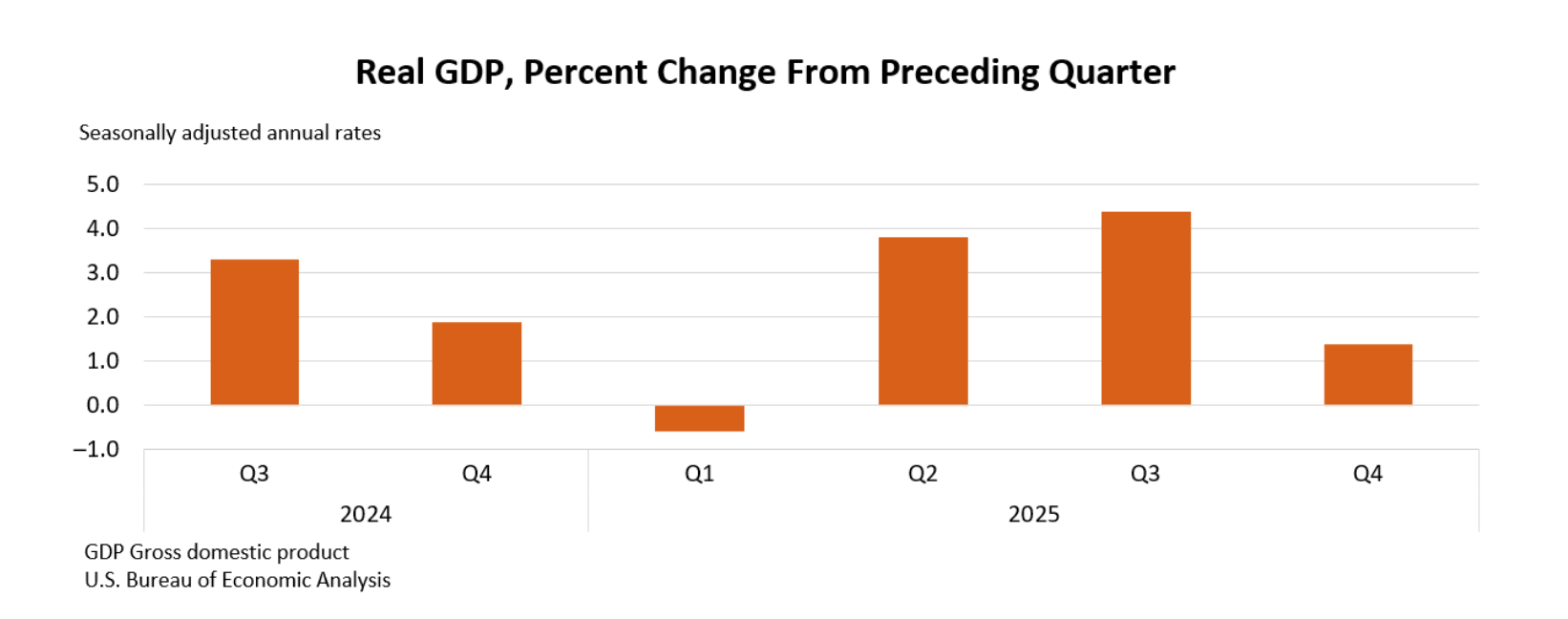

Growth of the US economy during the fourth quarter of 2025 slowed dramatically from a torrid pace in the second and third quarters, according to the Bureau of Economic Analysis Gross Domestic Product, 4th Quarter 2025 (Advance Estimate). Its key takeaways include:

RGDP, as reported by the Bureau of Economic Analysis’s advance estimate, increased at an annual rate of 1.4% in the fourth quarter, a sharp slowdown from the 4.4% pace recorded in the third quarter. The deceleration reflected a combination of factors, most notably the federal government shutdown in October and November and a pullback in consumer spending on goods. The shutdown alone accounted for roughly one percentage point of the decline in quarterly growth, underscoring the significant drag that disruptions in federal operations can have on overall economic activity.

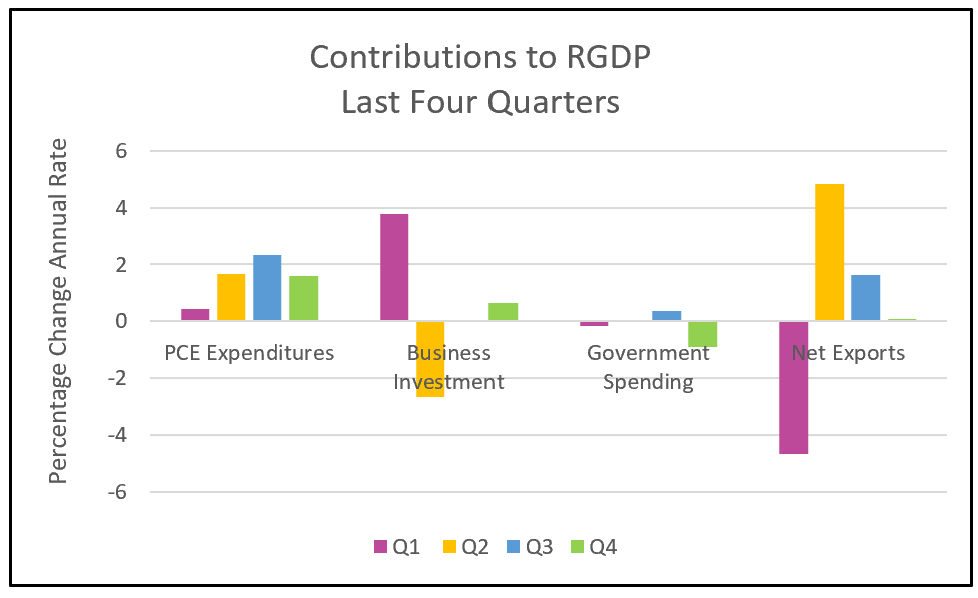

Despite the slower pace, consumer and business spending still accounted for the majority of fourth-quarter growth. Consumer spending expanded at a more moderate rate, resulting in a smaller contribution to RGDP. Notably, all of the increase in consumer spending came from services, particularly health care, while goods sales edged lower. Health care alone contributed 0.63 percentage points to the 1.4% overall growth rate, highlighting how dependent current expansion has become on a narrow set of service industries. A slight decline in imports provided a technical boost to output. However, falling government spending and weaker exports offset part of those gains.

Business investment rose 3.7% in the fourth quarter. Gains in gross private domestic investment were concentrated almost entirely in AI-related activity, masking weakness in other areas. Residential construction declined, as did spending on other structures, signaling softness in parts of the broader investment landscape.

Government spending fell sharply, with federal outlays dropping at a 16.6% annual rate in the fourth quarter, primarily due to the shutdown. According to the Bipartisan Policy Center, approximately 1.4 million federal employees went without pay during the government shutdown. Government shutdowns typically slow economic activity as furloughed workers reduce spending, though much of the lost output is generally recouped once employees return to work and receive back pay. As a result, economists expect a rebound in government spending during the first two quarters of 2026.

Looking at the broader picture, the economy proved resilient in 2025 despite significant headwinds. The year began with a modest contraction in the first quarter as imports surged ahead of tariff implementation. However, many tariffs were rolled back later by President Trump, and businesses adapted to shifting trade policies. The Federal Reserve, concerned about recession risks, lowered its benchmark interest rate, supporting demand for big-ticket items such as automobiles and helping propel stock markets to record highs. Rising asset values encouraged higher-income households—who have driven a large share of consumer spending—to continue spending.

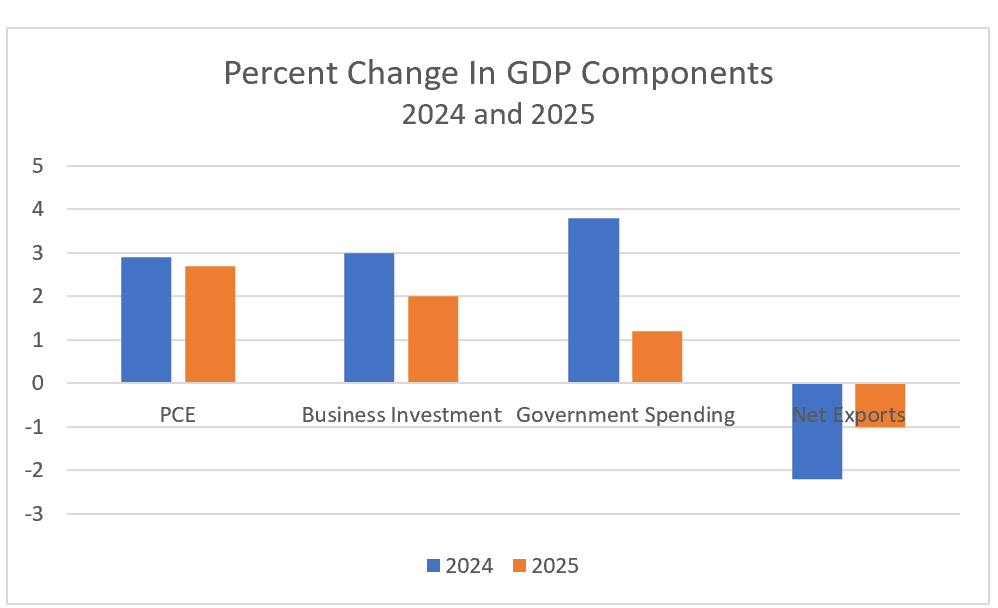

Even so, underlying private-sector momentum softened as the year progressed. Economists often focus on final sales to private domestic purchasers, which excludes government spending, trade, and inventory swings. This measure slowed from a 2.9% annual rate in the third quarter to 2.4% in the fourth quarter, and averaged 2.7% for all of 2025, down from 3.0% in 2024. Overall, RGDP increased 2.2% in 2025, compared with 2.8% in 2024 and 2.9% in 2023, reflecting slower growth across consumer spending (PCE), business investment, and government spending.

Inflation also firmed late in the year. The 12-month PCE price index rose 2.9% in the fourth quarter, up from 2.5% a year earlier, and accelerated from 2.8% in the third quarter. For 2025 as a whole, inflation averaged 2.6%, matching 2024’s pace, though the core PCE price index increased from 2.8% in 2024 to 2.9% in 2025. The pickup in inflation between the third and fourth quarters provides evidence that tariffs may have exerted upward pressure on prices, even as overall economic growth slowed.

The Bureau of Labor Statistics will release its February Employment Summary on March 6th. Economists and investors will be most interested in whether February’s gains in hiring mirror the surprisingly large increase in payrolls in January. (See Higher Rock’s summary.) We will provide a timely summary and analysis of each report shortly after its release. Also, be sure to look out for our forecasts for RGDP, employment, and inflation for 2026, as well as a review of how our 2025 predictions performed, later this month.