The inflation figures from the Bureau of Labor Statistics (BLS) Press Release: Consumer Price Index (CPI) – May 2026.

Inflation accelerated again in May, extending a troubling trend that has increasingly strained household finances. While most categories of goods and services experienced relatively modest price increases, a sharp rise in energy costs pushed overall inflation to its highest level in three years and further eroded consumers’ purchasing power.

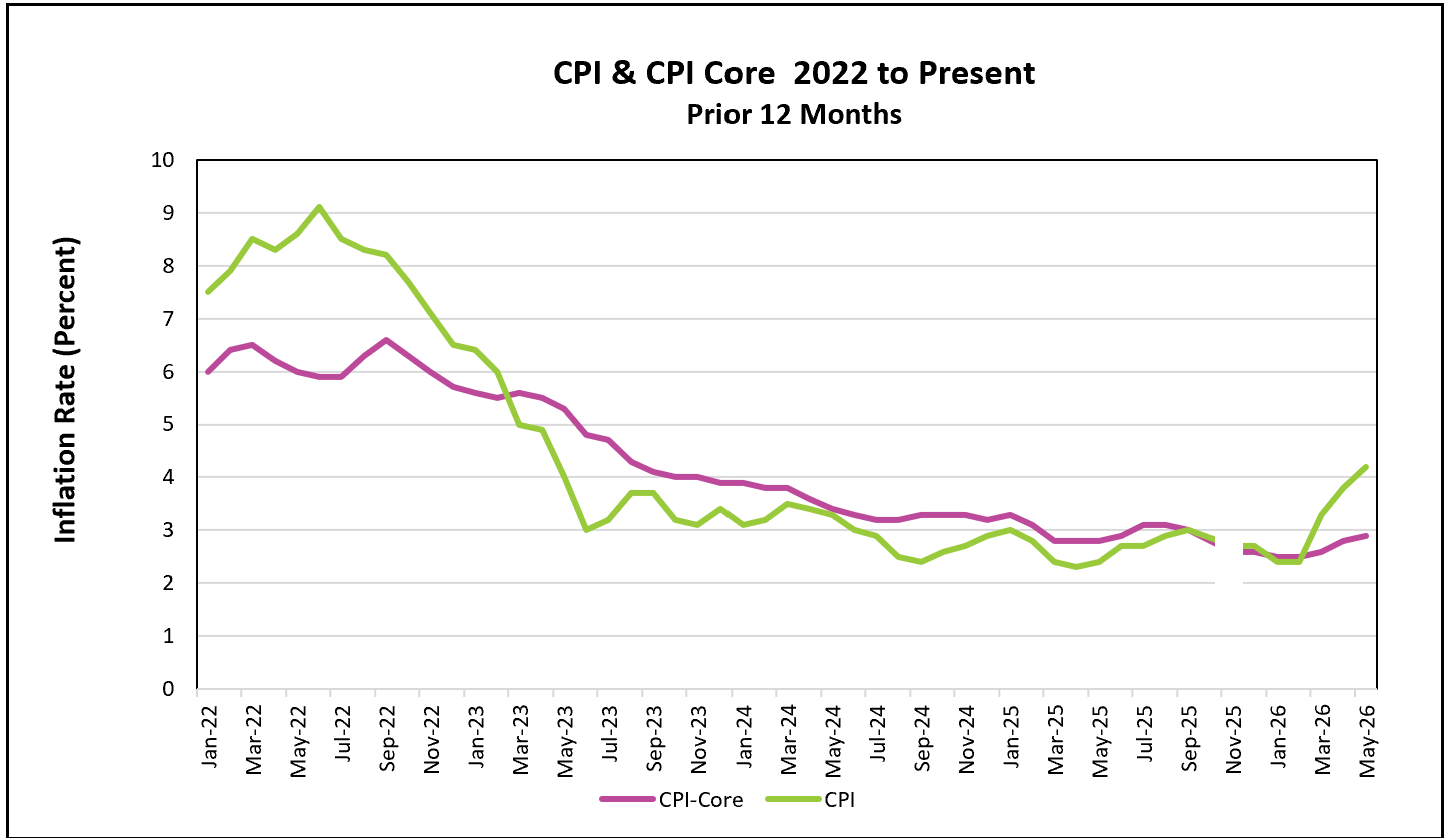

Prices increased 4.2% over the past 12 months, more than double the Federal Reserve’s 2% target. Energy-related costs accounted for more than 60% of the increase, underscoring the significant impact of geopolitical tensions and supply disruptions on household budgets. The 12-month inflation rate has now accelerated for three consecutive months, although the month-over-month increase slowed, potentially signaling that energy-related inflation may be nearing its peak.

The inflation surge comes at a difficult time for many Americans. Real hourly wages fell 0.1% in May and are 0.7% lower than a year ago. As a result, many households are finding that their paychecks purchase fewer goods and services than they did previously.

When wages fail to keep pace with rising prices, consumers generally have three options: reduce savings, increase borrowing, or cut spending. Many households are already exhausting the first two options. The personal savings rate has fallen to historical lows, while credit card delinquencies continue to rise. Consequently, many consumers have begun reducing discretionary spending in an effort to make ends meet.

The deterioration in purchasing power has contributed to growing consumer anxiety. The University of Michigan’s consumer sentiment index recently fell to its lowest level in years, with inflation cited as the primary source of concern. Perhaps more troubling, many consumers now expect inflation to remain elevated for years. When inflation expectations become embedded in the economy, consumers and businesses begin making decisions under the assumption that prices will continue rising, increasing the risk that higher inflation becomes self-sustaining.

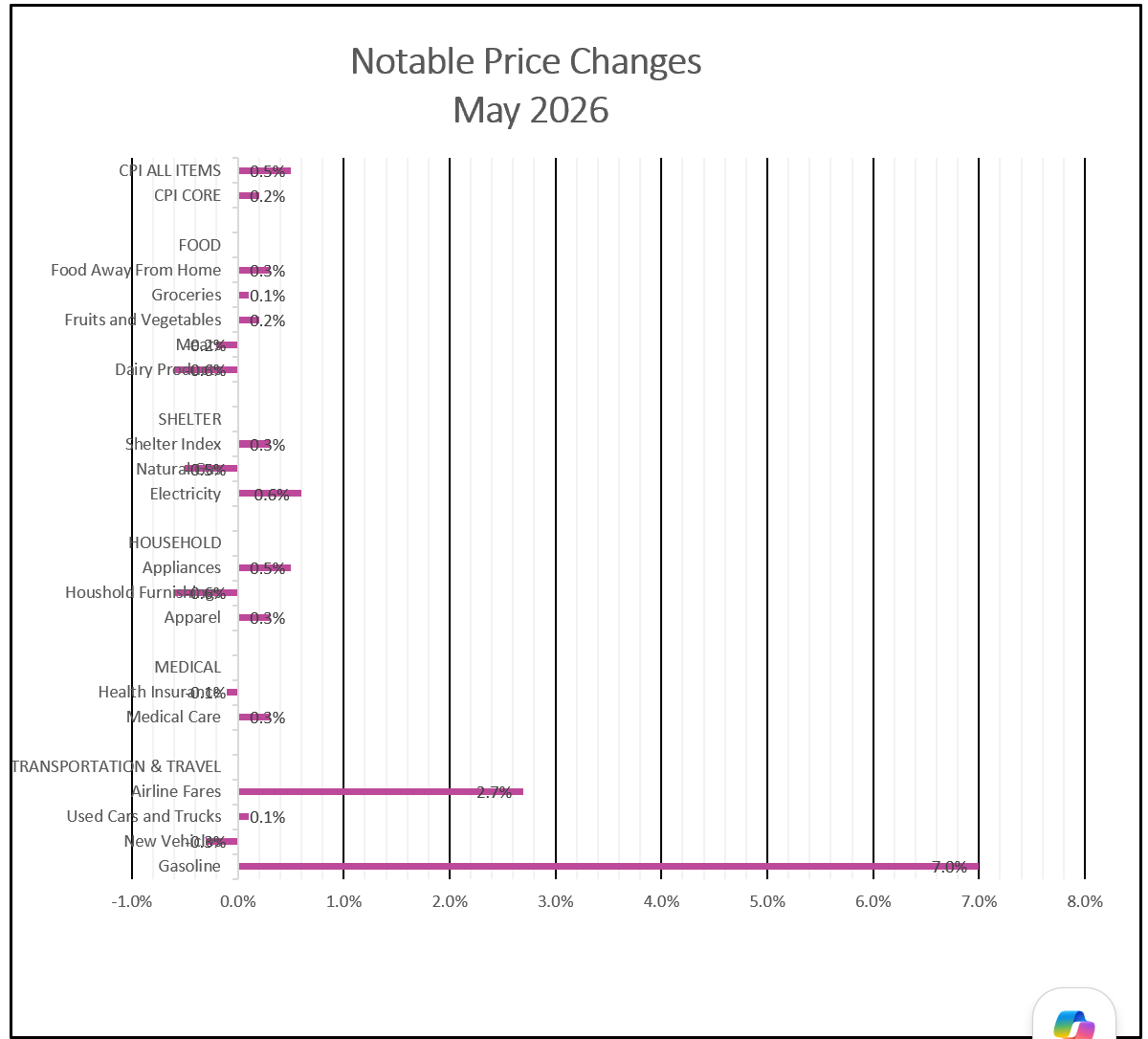

The recent inflation surge has been overwhelmingly concentrated in energy markets. Gasoline prices increased 7% in May and have risen approximately 70% over the past 12 months. Nationally, gasoline currently averages $4.15 per gallon, substantially higher than the $2.92 average recorded before the United States and Israel launched military operations against Iran. While today’s prices remain below the May peak of $4.56 reported by AAA, fuel costs continue to place considerable pressure on household budgets.

The sharp reversal is particularly notable because falling gasoline prices helped restrain inflation throughout 2025. Gasoline prices declined 3.4% last year, providing relief to consumers and helping offset price increases elsewhere in the economy. Today, gasoline is one of the primary drivers of rising inflation.

Despite the concerning headline inflation figures, there are signs that underlying inflationary pressures are not as severe as the CPI suggests.

The core inflation rate, which excludes the often-volatile food and energy categories, increased 2.9% over the past year. While above the Federal Reserve’s target, it is only slightly higher than the 2.6% reading recorded at the end of last year.

Many economists and policymakers view the core index as a more reliable indicator of long-term inflation trends because it is less susceptible to temporary swings in commodity prices. Encouragingly, several categories experienced outright declines in May. Prices for new vehicles, motor vehicle insurance, and household furnishings all decreased during the month. Grocery prices rose only 0.1%.

The relative stability of core inflation provides hope that overall inflation could moderate if energy markets stabilize and shipping routes normalize following the eventual reopening of the Strait of Hormuz. However, economists caution that inflationary pressures could become broader and more persistent if the conflict continues for an extended period. Businesses facing higher transportation, energy, and input costs may eventually pass those expenses on to consumers.

The inflation report arrives at a pivotal moment for the Federal Reserve. Kevin Warsh began his tenure as Federal Reserve Chair last month and will preside over his first policy meeting on June 16-17. He has previously expressed a willingness to lower interest rates, but many policymakers remain hesitant.

The debate within the Federal Reserve has become particularly intense, as inflation remains above target while the labor market remains resilient. Under normal circumstances, persistent inflation would argue for tighter monetary policy. However, the moderation in core inflation has reduced the urgency for immediate rate increases.

Many economists now believe the Federal Reserve is less likely to raise rates because core inflation has remained relatively stable despite the surge in energy prices. Nevertheless, some policymakers worry that inflation could become more entrenched if expectations continue rising and businesses begin passing higher costs through the broader economy.

Chair Warsh faces a challenging task. He must reassure financial markets that the Federal Reserve remains committed to price stability while managing pressure from President Trump, who has advocated for lower interest rates. The central bank’s credibility may depend on its ability to convince investors and consumers that inflation will eventually return to target.

If inflation remains elevated for an extended period, the broader economy could face increasing recession risks.

Consumers have already experienced a decline in purchasing power and many have reduced spending accordingly. If these spending cutbacks become widespread, aggregate demand could weaken significantly. Businesses facing slower sales may reduce hiring or eliminate jobs, causing unemployment to rise.

At the same time, persistent inflation tends to keep interest rates elevated. Higher borrowing costs increase the expense of purchasing homes, vehicles, and other large-ticket items while discouraging business investment. Together, weaker consumer spending and reduced business investment can create conditions for slower economic growth.

For now, the inflation story remains largely an energy story. The relative stability of core inflation offers reason for cautious optimism. However, policymakers will continue monitoring whether higher energy costs begin spreading throughout the broader economy. The longer energy prices remain elevated, the greater the risk that temporary price pressures evolve into a more persistent inflation problem.

Looking ahead, policymakers are likely to remain cautious. The Federal Reserve is expected to hold steady until there is greater clarity on the duration and scope of the conflict and its economic impact. Meanwhile, attention will turn to the Bureau of Economic Analysis’s upcoming Income and Outlays report, scheduled for release on June 25. This report will offer critical insight into how rising energy prices are affecting consumer spending. Higher Rock will provide a detailed analysis shortly after its release.