The Bureau of Economic Analysis published key April statistics in its Personal Income and Outlays report. Here are the key highlights of its report.

The latest data on consumer spending, income, and inflation paint a concerning picture of an economy dependent on households that are showing signs of financial strain. While consumer spending continued to rise in April, much of the increase reflected higher prices rather than stronger demand, raising questions about the sustainability of economic growth in the months ahead.

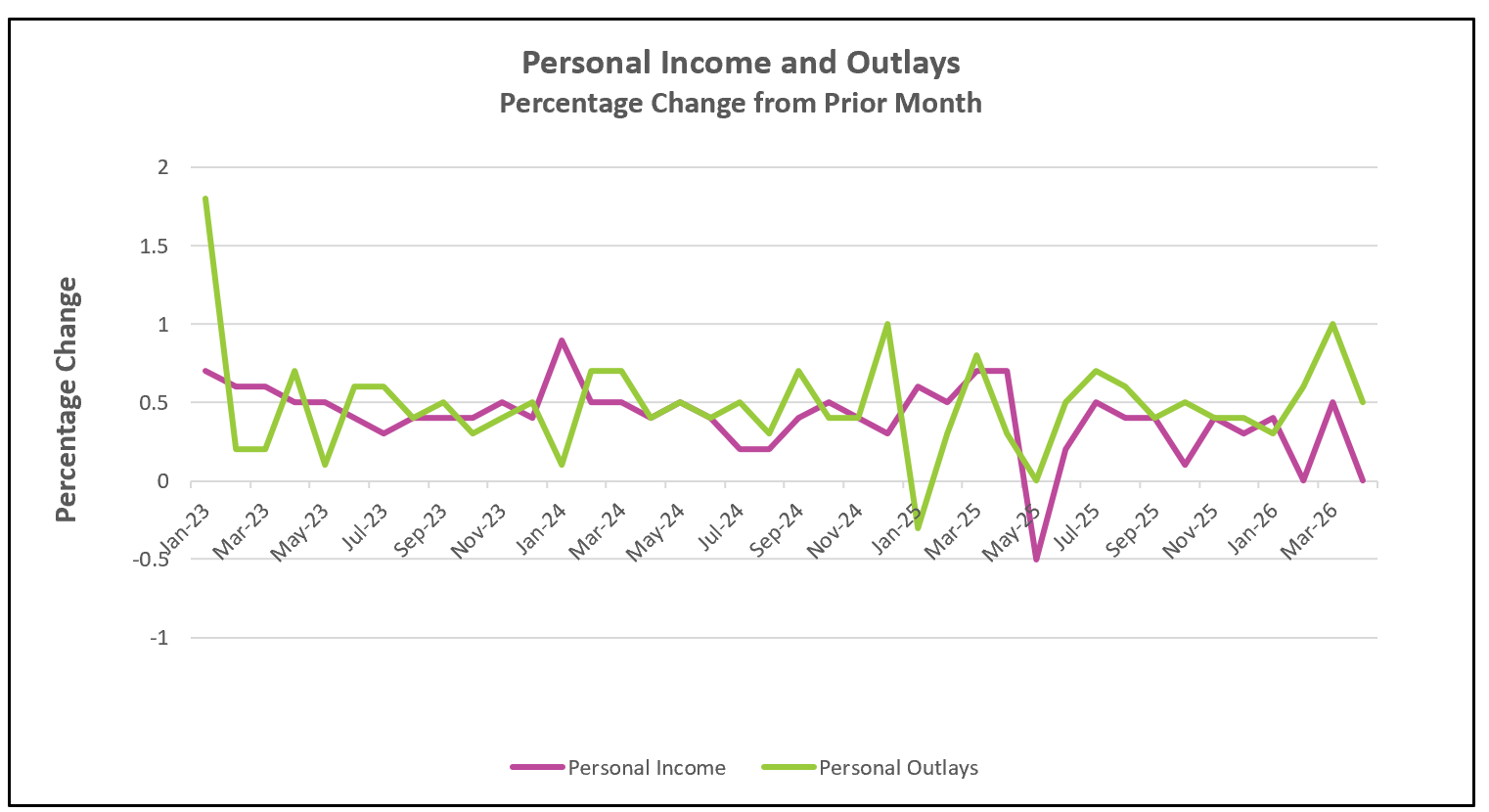

Consumer spending, which accounts for more than 70% of U.S. economic activity, increased 0.5% in April. However, after adjusting for inflation, spending rose only 0.1%, indicating that households purchased little more than they had the previous month, despite spending more. At the same time, personal income remained unchanged, and after adjusting for inflation, disposable income fell by 0.5%, further straining household budgets. April marked the third consecutive month of declining real disposable income. When prices rise faster than income, purchasing power erodes, leaving many families with less real income available for discretionary purchases.

As consumers struggle to keep up with rising costs, they are increasingly relying on savings and credit. The personal savings rate fell to its lowest level in three years, while credit card balances climbed to record levels. (WSJ - May 29, 2026) Financial stress is becoming more apparent, as payment delinquencies have reached their highest level in 15 years. These trends suggest that many households are stretched thin. Consumers generally prioritize mortgage payments, food, healthcare expenses, and auto loans before paying credit card bills, making rising credit card delinquencies a strong indication of growing financial pressure.

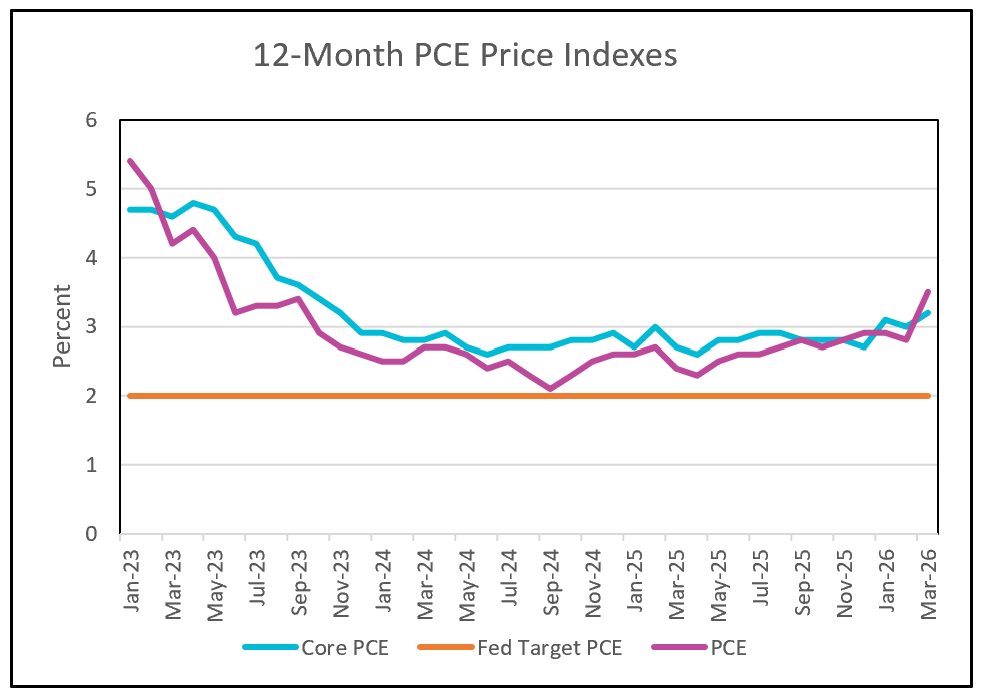

Inflation remains a major concern. Although the Personal Consumption Expenditures (PCE) Price Index decelerated modestly in April, prices remain elevated on a year-over-year basis. The overall PCE price index increased 3.8% over the past 12 months, the highest reading since May 2023 and well above the Federal Reserve’s 2% inflation target. Inflation has now remained above that target since early 2021. The core PCE index, which excludes food and energy prices, rose 3.3% over the past year, reaching its highest level since October 2023. The elevated core inflation rate suggests that inflation is becoming more entrenched as higher tariffs and energy costs continue to work their way through the broader economy.

The combination of slowing real consumer spending, falling real income, rising debt burdens, and persistent inflation does not bode well for future economic growth. Reflecting these concerns, the Commerce Department recently revised its estimate of first-quarter economic growth downward from 2.0% to 1.6%. (BEA GDP Second Estimate) While business investment—particularly spending related to artificial intelligence—has helped support economic activity, consumers remain the primary engine of the U.S. economy. Any sustained slowdown in household spending could have significant consequences for growth and employment.

These developments are also creating challenges for monetary policymakers. Despite accelerating inflation, Federal Reserve officials have resisted raising interest rates. Policymakers have argued that several recent inflationary pressures—including the COVID-19 pandemic, the war between Russia and Ukraine, and President Trump’s tariffs—represent supply-side shocks that eventually fade. Historically, inflation caused by supply disruptions often subsides once those disruptions ease.

However, as inflation remains elevated, a growing number of policymakers are advocating for tighter monetary policy. The debate has become even more complicated following the swearing-in of Kevin Warsh as Federal Reserve Chairman. President Trump nominated Warsh in part because of his willingness to support lower interest rates. Yet in today’s inflationary environment, Warsh may find it difficult to convince fellow policymakers that rate cuts are appropriate while inflation remains far above the Federal Reserve’s target.

The outlook for consumers and the broader economy remains uncertain. Rising prices, weakening purchasing power, declining savings, and growing financial stress all point to a consumer sector that is becoming increasingly fragile. With households accounting for most economic activity, their financial health will be critical to determining whether the economy can maintain momentum in the second half of the year.

Attention now turns to the labor market. The Bureau of Labor Statistics will release May’s payroll employment and unemployment data on Friday, providing important insight into whether businesses continue to hire despite mounting economic pressures. Higher Rock will publish a detailed summary and analysis shortly after the report’s release.